A-Basler/iStock via Getty Images

Almost two years ago, I covered Chr. Hansen (OTCPK:CHYHY) for the first and only time. Back then, the stock was clearly overvalued. In the meantime, the stock declined almost 20% and we must question once again if Chr. Hansen could be a good investment right now. In the following article I will explain, why Chr. Hansen clearly has a wide economic moat and is a great company. But we will also look at the stock price again and try to determine if Chr. Hansen could be a solid investment right now.

Wide Economic Moat

In this article, we start by describing the wide economic moat again. As I mentioned in my last article, the economic moat of Chr. Hansen is based on the company’s patents and switching costs. According to the company’s Annual Report 2020/21, Chr. Hansen has around 3,100 patents as well as 3,000 trademarks and in fiscal 2020/21, the company filed for 22 new patents.

Aside from the patents, the economic moat is stemming especially from the switching costs, which I described in my last article:

Chr. Hansen’s wide economic moat mostly stems from the switching costs the company has. First of all, Chr. Hansen is working with its customers and creating individualized solutions, which makes it difficult for the customers to switch to a competitor as the customers not only have to go through the process of finding an individualized solution once again. It is also uncertain if a competitor will be able to offer the same individualized solution as Chr. Hansen.

Aside from the individualization, the switching costs are so powerful as Chr. Hansen is producing a product that is very important for the end result, but makes up only a small fraction of the overall costs. The products of Chr. Hansen, for example, determine the color of food products, as well as beverages and the color, is extremely important as it plays an important role in the perception of the quality and has a huge influence how the end customer sees the product. Changing the color could be devastating for any product. Chr. Hansen’s products also determine taste and texture and changing these is similar dangerous as changing the color. A change in color, flavor, or texture might lead to fewer customers and every producer will be hesitant to change these aspects. And while the ingredients of Chr. Hansen have a huge influence on the end product, they make up only a very small fraction of the overall costs. When considering the costs for cheese production for example, the cultures and enzymes are responsible for only 1-2% of the total costs and the savings by switching to a competitor would be very little. Hansen’s products have a high benefit/cost ratio and this makes switching costs usually very high and creates a powerful moat around a business.

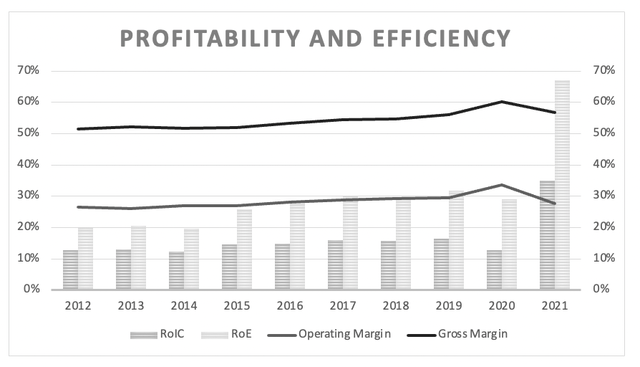

We can also look at the numbers, which will underline that Chr. Hansen has a wide economic moat. First, the company increased gross margin during the last decade while operating margin was more or less stable during the last 10 years.

Author’s work (based on numbers from Morningstar)

And not only were gross margin and operating margin extremely stable, the company also reported a return on invested capital above 10% every single year during the last decade. The average RoIC during the last ten years was 16.18%.

Without much doubt, Chr. Hansen is innovation-driven, and the company is spending about 8% of its revenue on research and development and Chr. Hansen has more than 145 years of experience in microbial science. And right now, Chr. Hansen also has one of the industry’s largest culture collections with more than 40,000 strains.

Christian Hansen Investor Presentation

Growth

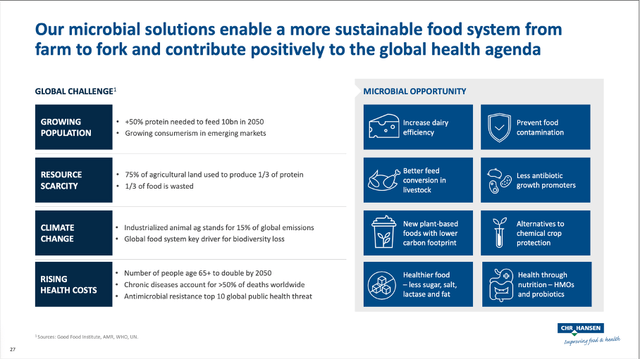

Chr. Hansen will not only profit from its economic moat, but also from several megatrends and from several global challenges, that must be met. The growing population for example, which will grow to about 10 billion people in 2050, will need 50% more protein and Chr. Hansen can also contribute by preventing food contamination. Other global challenges and drivers of growth for Chr. Hansen could be resource scarcity as well as climate change.

Christian Hansen Investor Presentation

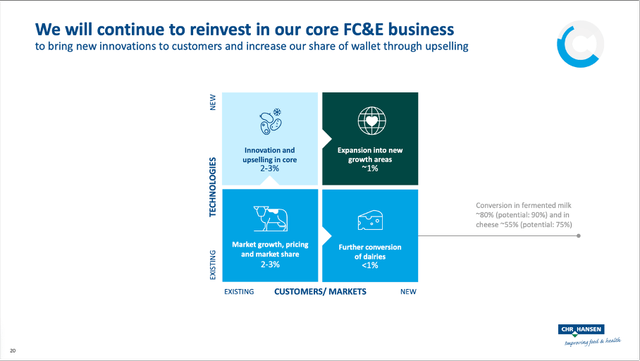

And of course, Chr. Hansen will continue to reinvest in the core business and aspects like innovation and upselling as well as the expansion into new growth areas will add to growth in the years to come.

Christian Hansen Investor Presentation

When looking at Chr. Hansen’s mid-to-long term ambitions, we find the targets for the years until 2024/25. The company is expecting organic revenue growth to be in the mid-to-high-single digits in the next few years and EBIT margin is also expected to increase over the next few years to at least 30%. The improvement is expected to be based on efficiency gains, scalability benefits and acquisition synergies.

Results

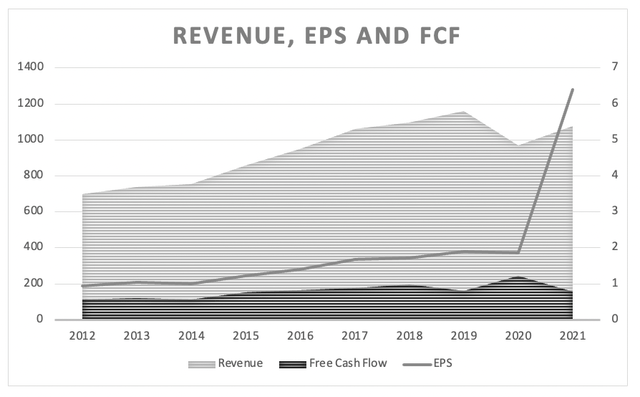

But when looking at the results in the recent past, we must be a little skeptic about the growth potential of Chr. Hansen. Don’t get me wrong, the results in the last few quarters were solid, but we saw not much growth. And Chr. Hansen clearly has a wide economic moat, but revenue even declined in the last two years and in the last five years, revenue increased only with a CAGR of 2.57%. Earnings per share also stagnated in the last few years (the results of the last fiscal year should be ignored as EPS for fiscal 20/21 was clearly an outlier).

Author’s work (based on numbers from Morningstar)

When looking at the results for the first half of fiscal 2021/22, revenue improved from €503.5 million in the first half of fiscal 2020/21 to €571.8 million resulting in 13.6% year-over-year growth (with organic growth being 12% in the first half of fiscal 21/22). Diluted earnings per share increased from €0.72 in the first half of fiscal 20/21 to €0.79 – resulting in 9.7% year-over-year growth. It remains to be seen, if Chr. Hansen can return on the path of growth again after some mediocre years in the past.

Balance Sheet

Chr. Hansen also has a solid balance sheet. On February 28, 2022, the company had current borrowings of €156.6 million as well as non-current borrowings of €834.3 million. When comparing the total debt to the total equity of €1,641.9 million, we get a debt-equity ratio of 0.60. While the debt-equity ratio seems acceptable, we also must point out that a huge part of assets is goodwill (€1,494.4 million). And when comparing the total debt to the operating income of the last four quarters (which was €316 million), it would take a little more than 3 years to repay the outstanding debt, which is also acceptable. But when summing up, Chr. Hansen has a solid balance sheet and there is no reason to worry.

Intrinsic Value Calculation

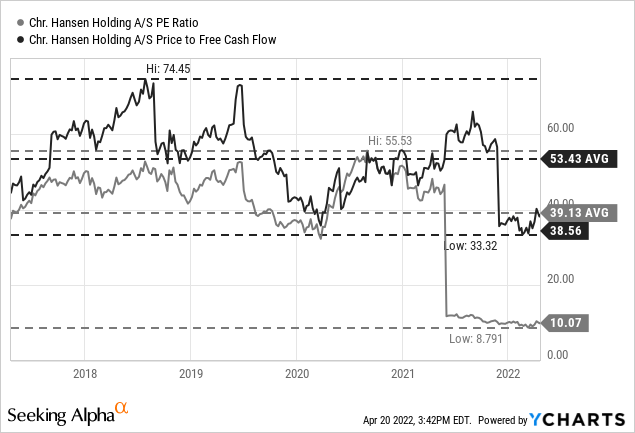

When trying to determine if Chr. Hansen is a good investment, we can start by looking at the price-earnings ratio. And when looking at that valuation multiple in the last five years, it seems like Chr. Hansen is an extreme bargain right now as the stock is trading for only 10 times earnings. However, these numbers are misleading, and we should look at the price-free-cash-flow ratio instead – and the picture is changing.

Chr. Hansen is trading for 38.5 times free cash flow right now and while this is one of the cheaper P/FCF ratios of the last five years and clearly below the 5-year average of 53.43, I have trouble seeing Chr. Hansen as a bargain. The picture we get so far is that Chr. Hansen has been extremely overvalued for several years and just the fact, that Chr. Hansen is trading for cheaper valuation multiples than in the last few years doesn’t make the stock a bargain.

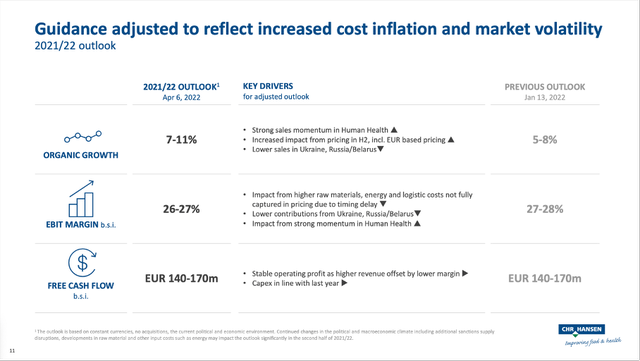

And that assessment can be confirmed by using a discount cash flow calculation. According to its own guidance, Chr. Hansen is expecting free cash flow to be only between €140 million and €170 million. But let’s be optimistic and use the free cash flow of the last four quarters instead, which is €228 million.

Christian Hansen Investor Presentation

And let’s also ignore that Chr. Hansen has been struggling in the last few years and assume an optimistic 10% growth (which was a long-term target of Chr. Hansen in a past presentation) in the next ten years followed by 6% growth till perpetuity. When calculating with these assumptions, a 10% discount rate and 133 million outstanding shares, we get an intrinsic value of €56.88, and the stock is still overvalued – despite the recent drop.

Christian Hansen Investor Presentation

I must be honest: Although I consider 10% annual growth for the next decade being already a high and ambitious growth rate, I have trouble to come up with a realistic growth rate for Chr. Hansen. When looking at the past few years, 10% annual growth seems to be completely unrealistic as Chr. Hansen was struggling to keep its revenue and free cash flow even stable. But when looking at the years before, we can also see glimpses, that Chr. Hansen might be able to grow with a much higher pace.

We only have data for about 15 years, as Chr. Hansen is only listed on stock exchanges since 2010. And that is not enough data for a clear picture, but you know me as a rather cautious person, and I would not calculate with higher growth rate than 10% for Chr. Hansen. And even if we use higher growth rates (14% for example), the stock is still not a bargain, but fairly valued at best.

Conclusion

Chr. Hansen is a solid company with a wide economic moat, and it is also operating in a niche. But the stock is not a buy in my opinion as the premiums we must pay for the stock are just too high.