Teenager00000/iStock by using Getty Illustrations or photos

To start with, The News

IBM (NYSE:IBM) claimed effects on July 18th. Non-GAAP conquer by $.02 with EPS of $2.31, which was sensible. Income was about $15.5 billion, up around 9% YoY, which was also a defeat. Money was also up to just underneath $8 billion, and complete credit card debt (which include financing financial debt) was down $1.4 billion.

Looking ahead, there is certainly most likely additional good information. Earnings is expected to be up mid-one digits, possibly at the high conclude in the 7-9% vary. That involves opportunity forex headwinds, which are approximated to be about unfavorable six details. And finally, FCF is expected to be about $10 billion.

On the complete, this does not seem so undesirable. In fact, lengthy-phrase traders are most likely delighted, or at the very least content enough. But, there is plenty of darkness, and IBM isn’t really a amazing firm. At very best, it really is a maintain.

The Storm Clouds

Ironically, the strong U.S. dollar is hurting IBM. This is what I mean:

IBM can make a minor over 50 percent of its overall revenue outside the house of the U.S., with about 30% in Europe.

Moreover:

IBM CFO Jim Kavanaugh said in the company’s Q2 meeting contact that the amount at which the U.S. greenback has strengthened is “unparalleled.” He famous that in excess of 50 percent of the currencies that IBM hedges from have dropped by double digits when compared to the U.S. dollar so significantly this 12 months.

So, even though the $10 billion in FCF appears great, it really is down 4-5% from former guidance of $10.5 billion. That roughly strains up with the six level strike from currency headwinds. Hedging would not appear to be operating properly sufficient.

Now, we have a further problem, and it is really termed Russia. Like many other organizations, the extraction is outstanding:

IBM has suspended enterprise in Russia, which includes engagement with Russian clients, small business associates, suppliers, suppliers, resellers, builders and OEMs and is conducting an orderly wind-down of all small business there. IBM is carefully monitoring the war in Ukraine and has taken motion to secure shopper and inside operations and to proceed supply of products and solutions and expert services to clients around the globe.

Curiously, IBM failed to say “Russia” even the moment in the Q2 2022 press release. In some methods, that’s odd, but in other approaches, it is not major information at all. Right after all, Russia accounting for roughly .5% of IBM’s whole earnings in 2021. My rough math says that $28-30 million so it is sort of a footnote.

Introducing it all up, the most significant problem appears to be the solid greenback. I have noticed incredibly minimal about the influence of inflation, in phrases of inputs, these types of as labor and elements. As a substitute, it’s all about the currency itself. Of study course, items could adjust quickly and we are going to carry on to observe.

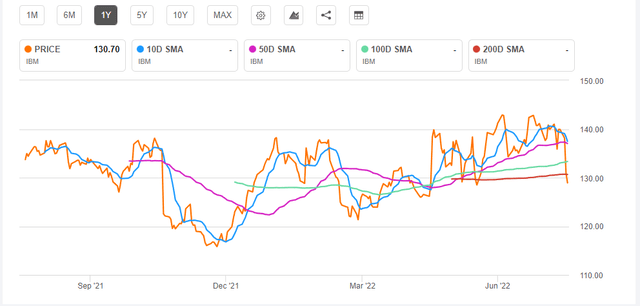

Momentum & Sentiment

I am not a enormous supporter of momentum considering the fact that it’s generally utilised for small-phrase trading, and solutions activity. However, I do fork out interest when there’s a vertical fall to the bottom of the properly – plop!

IBM – Going Averages (Trying to get Alpha)

We are hunting straight down ideal now:

10D = (6%)

50D = (6%)

100D = (3%)

Of program, the quantities are not big, but the value is straight down, ripping as a result of all moving averages. That stated, there is certainly not a loss of life cross in this article because the 10-day, 50-day and 100-day are all higher than the 200-working day SMA.

So, we’ll be seeing this as very well. But, at minimum on the surface area, there’s been a warning shot fired. Sentiment appears to be turning adverse listed here.

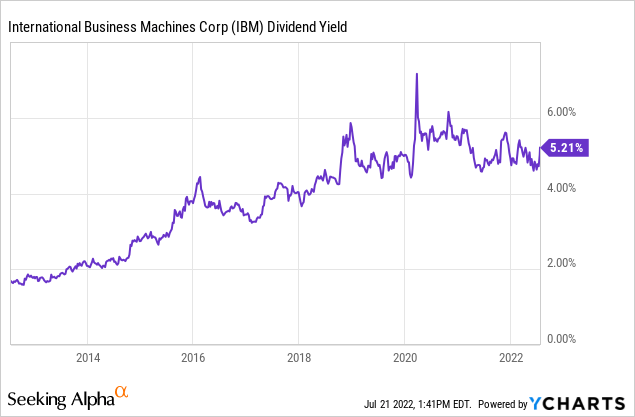

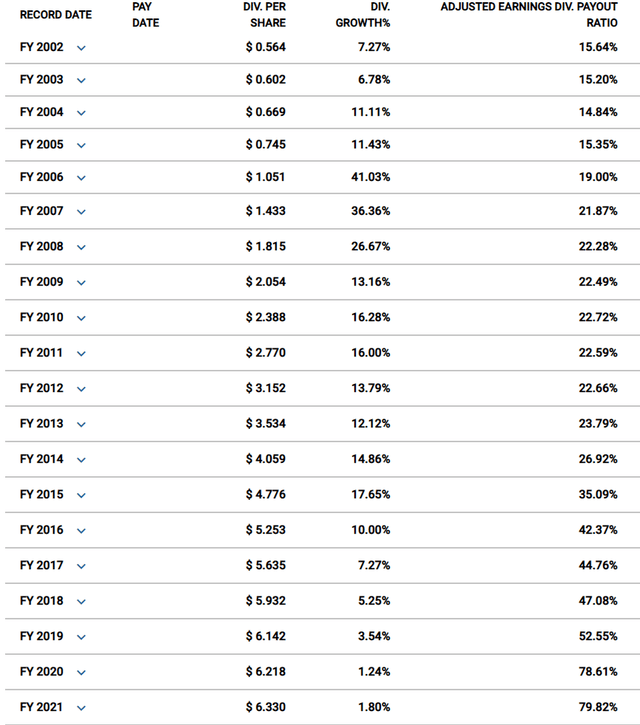

Very good News & Terrible Information About The Dividend

This is the fantastic news in a single easy chart:

In this natural environment, a produce of 5.2% is definitely pleasing. And, for prolonged-time traders, it’s pleasant to get compensated to keep. In common, for decades and a long time, that dividend has been creeping upwards.

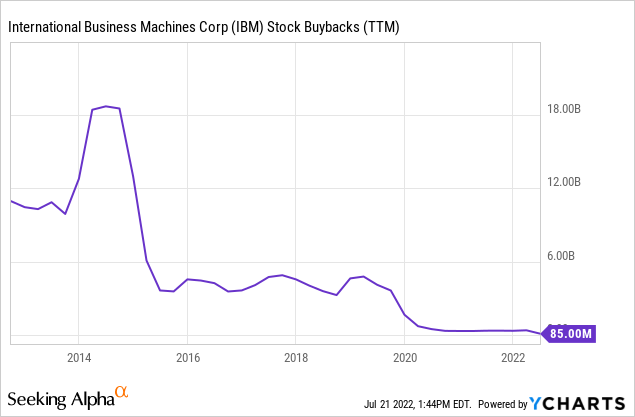

But, is this from frequent “sugar” injections? Take into account IBM’s buybacks.

Though the buybacks have declined noticeably, billions and billions were burned to juice EPS but also hold the dividends flowing. By cutting down the shares, IBM was able to retain the expansion in dividends.

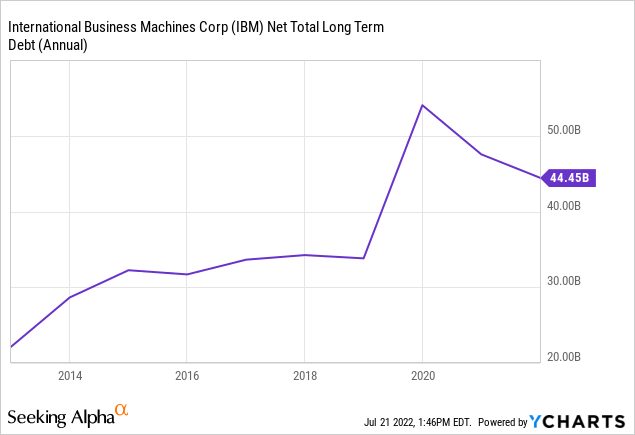

Of course, the credit card debt image is cloudy owing to Kyndryl (KD) and also financing personal debt. But, what matters is that in normal, IBM has piled on debt. Pushing out KD helped to regulate that debt a little bit. What issues listed here is uncomplicated. IBM stored the dividend large, and rising, through buybacks and financial debt. Said yet another way, management utilized economic engineering.

But wait around, you can find much more.

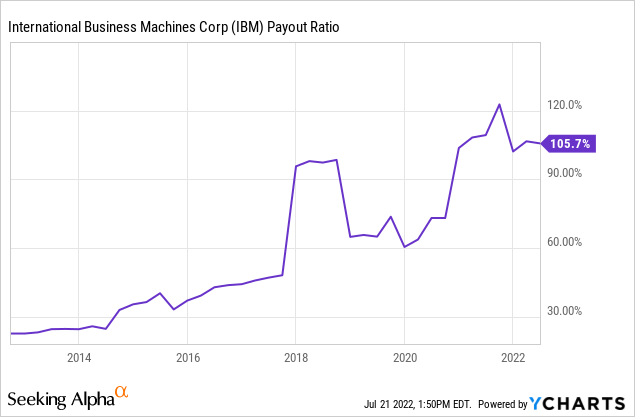

Generally, what we are seeing is a relentlessly rising payout ratio. IBM proceeds to grow the dividend, and preserve its remarkable progress streak, but the expense is large. Here’s one more watch of the trouble:

IBM Payout Ratio (FASTgraphs)

Like most of my examination, I am not on the lookout for perfection. That is, the dissimilarities involving YCharts and FASTgraphs really don’t each me. We’re hunting for converging proof. Each individual tool calculates factors a bit in a different way, in my encounter. What issues is the very noticeable pattern. Bottom line: IBM has gone from remaining a conservative dividend machine to a stretched rubber band. Who is familiar with if it will snap. You will find stress, even strain.

Wrap Up

Roughly talking, IBM appears to be to be navigating the present-day surroundings rather well. The business enterprise is experiencing macro challenges, specially forex headwinds, but it really is unquestionably extra focused now. With KD in the rearview mirror IBM is setting up to get extra significant about core competencies, like the hybrid cloud and synthetic intelligence. Set a further way, IBM isn’t really going absent.

On the other hand, the company would seem to still be trapped in the earlier. This just isn’t a nimble organization. It can be like an outdated “smokestack” business enterprise but in IT alternatively of industrial production. It really is also attempted monetarily engineer its way to success. This has been unsuccessful in my impression.

On the surface area, a single brilliant spot has been the dividend. The generate is high, and IBM is a dividend champion. But, they have loaded up on personal debt in excess of the yrs, and the payout ratio has been unpleasant. Frankly, I see hazard in the dividend. At a minimum amount, I really don’t see a lot advancement in the dividend. For many traders, that’s properly appropriate. I understand, but then it makes IBM anything of a bond proxy. That’s not what I find satisfactory, but I see why other folks want it that way.

Adding it all up, I see IBM as a hold. It really is fantastic for dividend buyers and earnings investors, I suppose. But, it really is very substantially a “has been” in terms of substantial growth, even with A.I. and the cloud. Also, in complete disclosure, I bought out of my past IBM shares back again in early 2022. I’m not shorter, but I’m absolutely not acquiring.